Solid Power: Innovative Battery Technology Driving Industry Forward (NASDAQ:SLDP)

[ad_1]

Mykola Pokhodzhay/iStock via Getty Images

Background and Update

Solid Power (NASDAQ:SLDP) has built one of the most impressive next-generation lithium-metal batteries. The company has partnered with OEM players, Ford (F), BMW (OTCPK:BMWYY), and SK Innovation (KRX: 096770). In the past, I have covered Solid Power and its partnerships with these companies. One of Solid Power’s main competitors, QuantumScape (QS), has also seen similar early success. QuantumScape has had many early successes within the lithium-metal battery space. Other battery companies can’t compete because of Solid Power’s technological advantage, from battery testing to solid-state cells. Batteries are a complicated space, so I found a Professor from Harvard to explain the concept.

A lithium-metal battery is considered the holy grail for battery chemistry because of its high capacity and energy density. But the stability of these batteries has always been poor

-Associate Professor of Materials Science Xin Li

(Source)

The difference between the two battery compositions is simple on the surface. Lithium metal can sort more energy because of the nature of the lithium anode in the battery. This allows for higher energy density as well as increased capacity. On the other hand, lithium-ion batteries don’t use pure lithium anodes, which can decrease conductivity, which leads to energy inefficiency. With the emergence of commercialized lithium-metal batteries, the old lithium-ion bellwether is looking to be replaced.

With less reliance on nickel, cobalt, and copper, companies can exit the controversial industries providing necessary natural resources. Despite the recent surge in lithium prices, it will likely be the metal of choice for producers. This is due to the strong early battery cell cycle test results, which suggested increased electric vehicle range, longer battery life, and faster charging.

Business Strategy Presents Promising Growth Verticals

Future business partnerships within the battery space should organically occur. Many traditional ICE OEMs need a solid-state EV partner to easily transition their fleet to electric technology. Manufacturers need Solid Power’s technology and the unique vertical scale the company operates on. This begins with its battery testing technology to the individual production of its own cathode and anode materials.

New facilities and continued operational improvement have been sourcing investments from various institutions. This will prove vital because it takes money and resources to produce these batteries at an industrial scale for electric vehicle use.

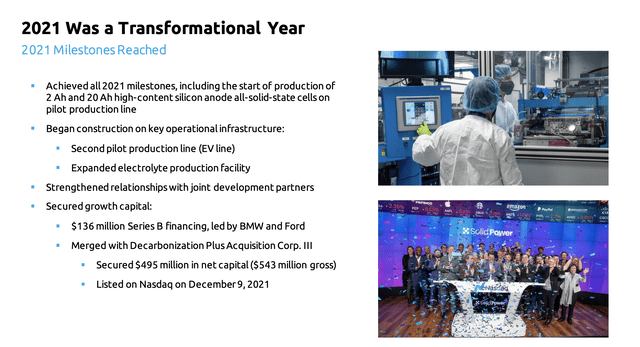

Solid Power Full Year 2021 Earnings Presentation

Risks to the Growth Thesis

The overall risks to Solid Power’s technological moat are relatively low. The primary risk I see to the company’s growth is the instability of the public markets. Recently, batteries have been selling off due to the tech correction, which has spread its way into other industries and technologies. Solid Power is unprofitable and will be for some time, which is unfortunate because it discourages investors who would typically invest. Investors should look at Solid Power as a risky investment and not a fundamentally appreciating asset.

Using Guidance as Basis for Valuation

The guidance looks promising and Solid Power is well-positioned to benefit in 2022. Battery sales will continue to increase, offsetting any incoming CapEx costs. Solid Power’s technology will unlock the true value of shares even in the face of increased commodity costs.

Capital expenditures should continue to accelerate. However, there will be revenue that will help offset those costs. The cell and electrolyte production facility will be vital to keeping costs down because other battery companies have seen pricing pressures that Solid Power has not. This will de-risk the company’s supply chain and ensure that its micro milestones will help it achieve its overall macro thesis of serving the global electric vehicle market.

Conclusion and Rating

Solid Power has made significant advancements past its IPO phase and shows actual growth to enable shares to trend higher. Due to various technological and business strategy factors, I re-rate Solid Power to a Strong Buy. I look forward to covering Solid Power in the future.

[ad_2]

Source link